Guide")

")

")

: Navigating New Visa Rules, Scholarships, and Top Ontario Colleges")

")

")

")

")

")

")

Introduction:

The terms “Travel Insurance” and “International Health Insurance” are often used interchangeably, but choosing the wrong one is a mistake that could cost you tens of thousands of dollars. As of 2026, the global travel landscape has shifted—medical costs in popular destinations like the U.S. and Japan have surged, and “border-less” living is more common than ever.

Whether you are planning a two-week safari in Kenya, a digital nomad stint in Bali, or a permanent relocation to the South of France, one question looms larger than your packing list: “How will I be protected if I get sick?”

In this comprehensive guide, we will dismantle the confusion between these two products, providing you with a data-backed roadmap to ensure you’re never left stranded.

The $100,000 Misunderstanding

Imagine this: You’re hiking in the Swiss Alps. You trip, shattering your ankle. A helicopter rescue costs $15,000, and the subsequent surgery and three-day hospital stay add another $45,000.

If you have Travel Insurance, you’re likely covered—provided the hike wasn’t considered an “extreme sport” exclusion. However, if you develop a chronic condition while living abroad and expect your travel policy to pay for ongoing monthly treatments, you’re in for a shock. Travel insurance is designed to “patch you up and send you home.” It is a safety net, not a healthcare plan.

According to IMARC Group (2025), medical expense coverage now leads all travel insurance types, accounting for 41.0% of the market share. Travelers are realizing that their domestic health plans (like Medicare in the U.S. or the NHS in the UK) often stop at the border.

Step-by-Step Solution: Choosing the Right Coverage

Navigating the insurance world doesn’t have to be daunting. Follow these four steps to identify your needs.

Step 1: Define Your Duration

- Under 3 Months: Standard Travel Insurance is usually sufficient. It covers short-term spikes in risk.

- 6 Months to 1 Year+: You are likely an expat or long-term traveler. You need International Health Insurance (IPMI).

Step 2: Evaluate Your “Home” Base

Are you keeping your domestic insurance? If you maintain your health plan at home, travel insurance acts as a bridge. If you are canceling your home plan, you need an international health plan that offers “comprehensive” care (preventative, chronic, and routine).

Step 3: Check Mandatory Requirements

In 2026, several regions (like the Schengen Area and parts of Southeast Asia) require proof of insurance. Ensure your policy meets the minimum medical limit—typically €30,000 for Europe or $50,000 for other regions.

Step 4: Audit Your Activities

If you are diving, skiing, or riding motorbikes, a standard health plan might cover the “medical” side, but only travel insurance typically includes the “search and rescue” or “repatriation” of remains.

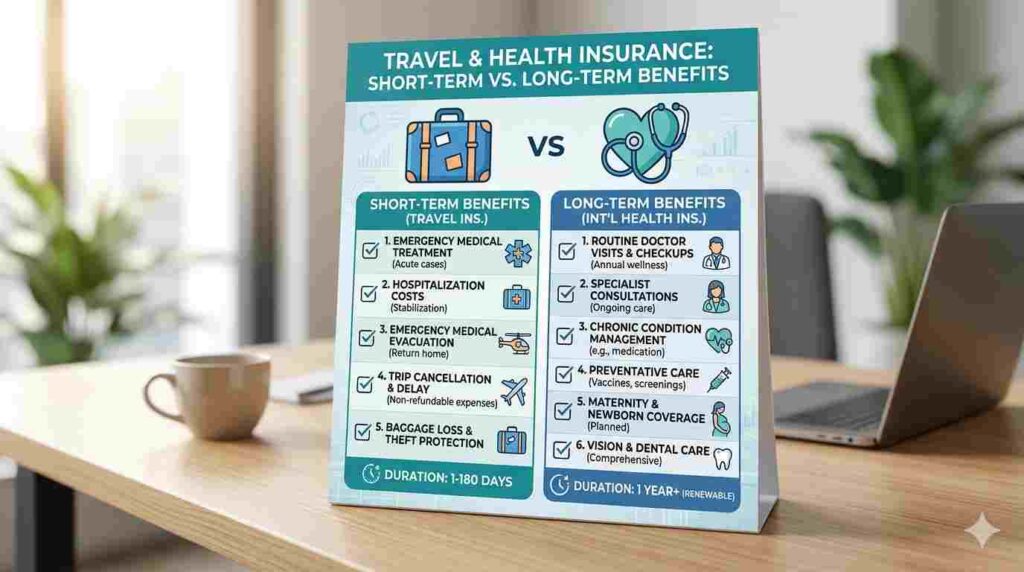

Comparison Table: At a Glance

| Feature | Travel Insurance | International Health Insurance |

| Best For | Holidays, Business trips, Vacations. | Expats, Digital nomads, Overseas workers. |

| Primary Goal | Emergency “stabilization” and trip protection. | Long-term health maintenance and wellness. |

| Medical Coverage | Only new, unexpected emergencies. | Routine care, chronic conditions, emergencies. |

| Trip Protection | Includes flight delays, lost luggage, theft. | Usually excluded (medical only). |

| Duration | 1 day to ~180 days. | 1 year (renewable). |

| Evacuation | Included (Return to home country). | Included (Transport to best local facility). |

| Cost Basis | Age, trip cost, and duration. | Age, area of cover, and medical history. |

Deep Dive: Travel Insurance vs. Health Insurance

What is Travel Insurance?

Travel insurance is a multi-risk package. It is designed to protect your financial investment in a trip. If your airline goes bust or your bag is stolen in Barcelona, travel insurance steps in.

Expert Quote: “Travel insurance is essentially ‘disruption insurance’ with an emergency medical rider attached. It assumes you have a home to go back to for long-term recovery.” — Senior Underwriter, Allianz Global.

Before you choose any policy for your travel insurance, it is important to discover what travel insurance actually covers.

What is International Health Insurance?

Also known as Expat Insurance, this is a lifestyle product. It functions like the health insurance you have at home but works globally. It covers:

- Inpatient & Outpatient care.

- Maternity and Newborn care.

- Prescription medications for chronic issues (e.g., high blood pressure, asthma).

- Cancer treatment and physical therapy.

Requirements and Checklist for 2026

Before you click “Purchase,” ensure your policy ticks these boxes:

The Essential Checklist

- [ ] Emergency Medical Limit: Minimum $100,000 (Recommended: $250,000 for the USA/Japan).

- [ ] Medical Evacuation: Minimum $250,000. (A private medevac flight from Asia to the US can cost $150,000+).

- [ ] Pre-existing Condition Waiver: Do you need coverage for a condition you already have?

- [ ] Repatriation of Remains: Covers the cost of returning your body home in a worst-case scenario.

- [ ] Crisis Response: Coverage for natural disasters or political unrest.

- [ ] Deductible/Excess: Is the “out-of-pocket” cost per incident or per policy?

Statistics & Data: The Reality of 2026 Travel

The 2026 insurance market has seen a sharp increase in “Medical-Only” travel policies.

- Average Cost of Medical Evacuation: According to Travel Care Air (2026), a transatlantic evacuation now averages $80,000–$150,000.

- Adoption Rates: Only 38% of US travelers purchase insurance, while 77% of UK travelers do (Condor Ferries 2025/26 data).

- The “Senior” Surge: Travelers aged 60+ now represent 31% of the insurance market, driving demand for higher medical limits.

Chart: Estimated Costs of Emergency Services Abroad (USD)

- Ground Ambulance (USA): $1,200

- Hospital Room (Japan): $800/night

- Air Ambulance (Regional): $25,000

- International Medevac (Long-haul): $120,000+

Expert Tips for Saving Money

- Check Your Credit Card: Approximately 29% of premium credit cards offer trip cancellation, but very few offer robust medical coverage. Use the card for the “trip” part and buy a “Medical-Only” travel policy to save up to 50% on premiums.

- Annual Multi-Trip Policies: If you travel more than 3 times a year, an annual policy is almost always cheaper than buying individual plans.

- The “Schengen” Trick: If you only need medical coverage to satisfy a visa, look for “Visa-compliant” plans which are stripped of baggage/theft fluff to lower the price. Our the ultimate guide to the best insurance for Europe will explain further about this.

Common Mistakes to Avoid

- Assuming “Global” means “Including USA”: Most international health plans have two tiers: “Worldwide” and “Worldwide excluding USA.” The latter is significantly cheaper.

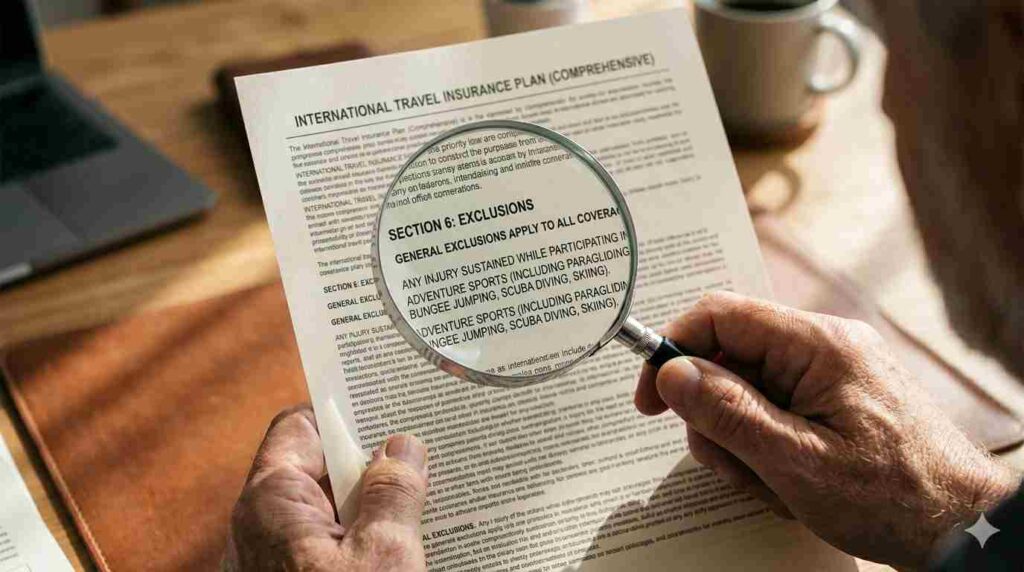

- Ignoring the “Adventure Sports” Clause: Standard travel insurance often excludes hiking above 2,500m, scuba diving deeper than 10m, or riding a scooter without a local license.

- Not Declaring Pre-existing Conditions: If you have diabetes and don’t declare it, any claim related to your blood sugar—even an accident caused by a dizzy spell—will likely be denied.

FAQs

Q: Does travel insurance cover COVID-19 in 2026?

A: Yes, most reputable providers now treat COVID-19 like any other unexpected illness, covering hospitalization and quarantine costs if medically mandated.

Q: Can I buy travel insurance after I have already left home?

A: Most companies require you to purchase before departure. However, “Digital Nomad” specialists like SafetyWing or World Nomads allow you to start a policy while already abroad, usually with a 48-72 hour waiting period.

Q: Does health insurance cover my lost laptop?

A: No. International Health Insurance is strictly medical. You would need a separate “Personal Effects” floater or a travel insurance policy for tech and gear.

Conclusion

The choice between travel insurance and international health insurance comes down to intent.

If you are a visitor, Travel Insurance is your best friend—it protects your wallet from the chaos of travel. If you are a resident (even a temporary one), International Health Insurance is your lifeline—it ensures you have access to quality care without draining your life savings.In 2026, the risk of traveling uninsured is no longer just a “bad luck” scenario; with medical inflation rising, it’s a financial gamble you cannot afford to lose. Check your policy today—before the wheels go up.

")

")

")

Guide")

{kind=link}